Episode 7 of 10: Format Revenue Profiles

Retail format is a primary lens for understanding business models and consumer propositions. The current landscape reinforces a wider trend: stronger growth in value and convenience formats relative to traditional super and hyper-market models.

Note: All retail format data is based on the head office location of the top 100 retailers.

The Scale Giants

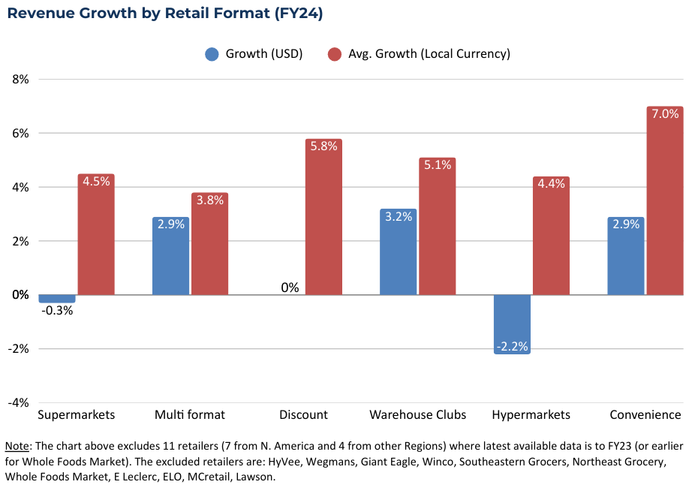

- Supermarkets: Remain the largest format, accounting for 36.3% of total top 100 revenues. Despite their scale, they lagged the grocery retail average growth in FY24, experiencing a minor share dilution as consumers shifted toward other models.

- Multi-format: The second-largest segment (30.3% share) with the highest average revenue per retailer ($78.5bn). Growth is currently supported by consumer demand for seamless online-to-offline (O2O) experiences. While gaining share in USD terms—driven by the strength of Walmart—the format’s average constant-currency growth of 3.8% actually lagged the overall top 100 average of 4.8%.

The Growth Drivers

- Convenience: The smallest format by revenue share (5.1%) but the fastest growing in constant-currency terms at 7.0%. Success is being driven by regional relevance, particularly in Asia Pacific, alongside consumer trends toward quick, proximity-based shopping missions.

- Discount & Warehouse Clubs: Both formats showed strong constant-currency growth (5.8% and 5.1% respectively). Discounters are successfully tapping into demand for affordable health and sustainability initiatives, while Warehouse Clubs leverage the appeal of bulk buying and membership loyalty in a cost-conscious environment.

- Hypermarkets: Facing the most pressure, this format's revenues declined by 2.2% in USD terms. Excluding the impact of high-growth Russian retailer Lenta, the average constant-currency growth for hypermarkets would be a mere 0.65%, highlighting severe pressure from more agile formats.

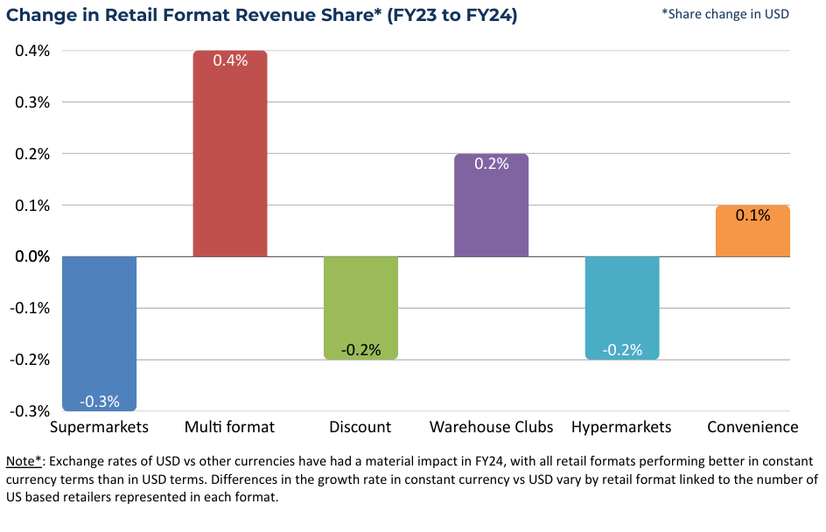

Format Share Shifts

Adjusting for currency impacts, Discount, Convenience, and Warehouse Club formats gained share in constant-currency terms. Conversely, Supermarkets and Hypermarkets both lost share as their growth lagged the top 100 average, with Hypermarkets feeling the specific impact of Target’s negative growth performance. Multi-format retailers led share gains in USD terms although growth was below average in constant currency terms indicating some share pressure on this basis.

Enjoying the series?

These materials may not be reproduced or distributed in part or in full, in any form or by any means, electronic or mechanical, including photography, recording, or any information storage and retrieval system now known or to be invented, without the express written permission of Comsensus Limited.